Though it may be finally starting to cool, inflation continues to bust budgets all over the United States. More than four decades have passed since the country has grappled with this magnitude of price increases.

But you know what folks didn't have in the '70s and '80s to help them weather inflation? Series I savings bonds — aka I bonds. These inflation-indexed government bonds were created back in 1998 specifically to help shield Americans' savings from rapidly rising prices.

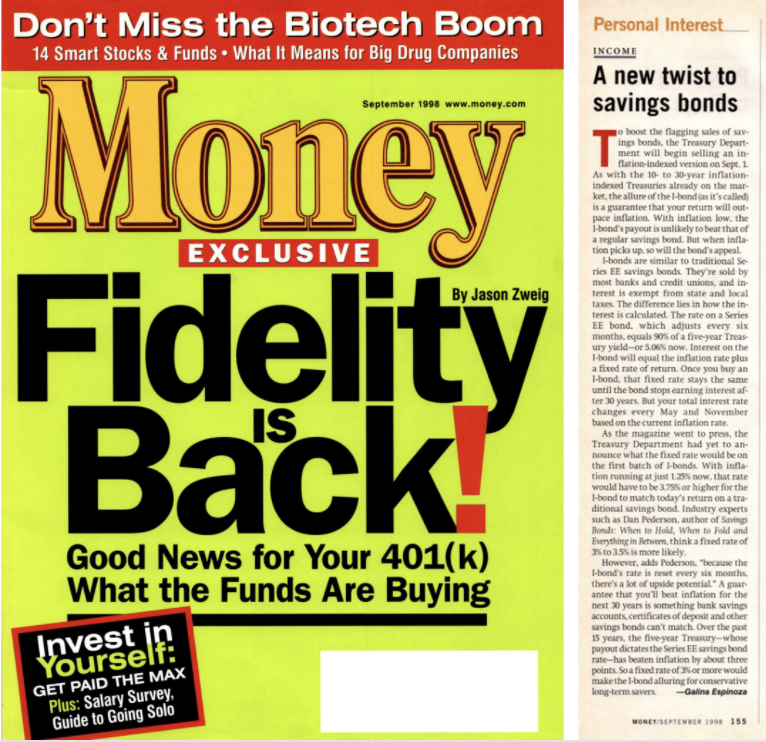

In our September 1998 issue, Money's Galina Espinoza covered the Department of the Treasury's release of the then-obscure bond, writing "the allure of the I bond (as it's called) is a guarantee that your return will outpace inflation."

That's because the interest rate on I bonds changes every six months based on fresh inflation data. So when consumer prices rise, so do the payouts on I bonds once (eventually) cashed.

In 1998, the annual inflation rate was just 1.6%, which is below the Fed's current target of 2% over the longer run. Needless to say, the inflation-protected bond didn't garner much fanfare at first.

But in November 2021, soaring inflation pushed the I bond interest rate first to 7.12%, then to an all-time high of 9.62% six months later. In less than a year, I bonds have become a hot commodity, with the Treasury Department selling nearly $30 billion worth.

The current annualized interest rate for I bonds is still 9.62%, but that historic rate is soon changing. Come November, the Treasury Department will announce a new rate, and it's expected to dip from the current high. But you can still lock in the record-setting interest rate for six months if you buy your I bonds before the end of October.

"With inflation low, the I bond's payout is unlikely to beat that of a regular savings bond," Espinoza wrote. "But when inflation picks up, so will the bond's appeal."

In other words, I bonds were made for this moment.

Read the story here, and see the cover below.

— Adam Hardy, reporter

Comentarios

Publicar un comentario